Bruno Farinelli

Bruno Farinelli

Shopify has earned its place as the big dog in ecommerce. The platform is used by online sellers in over 175 countries around the world, with 60% of Shopify stores estimated to be based in the United States.

That widespread use and popularity come at a cost: fraudsters see Shopify’s online businesses as an attractive target, with “high-risk” orders being the most appealing.

Here’s what businesses need to know to defend their businesses from the increased risk of Shopify fraud.

How Shopify Prevents Fraud

Transactions that are not authorized by the customer are referred to as fraudulent. A fraudulent transaction can result in a chargeback, which can cost you money.

As a Shopify store owner, you have built-in fraud detection tools at your disposal to help identify suspicious orders, depending on your plan and the type of transaction.

Fraud analysis

When Shopify businesses receive an order, the platform automatically scans the transaction for fraud indicators. The indicators can include information such as:

- Whether the credit card used for the order passes AVS checks

- Whether the customer provided the correct CVV code

- Details about the IP address used to place the order

- Whether the customer tried to use more than one credit card

The indicators can be used to investigate an order that you think might be fraudulent. Businesses can easily evaluate their Shopify transactions for fraud by following these three straightforward steps.

1. View the fraud analysis

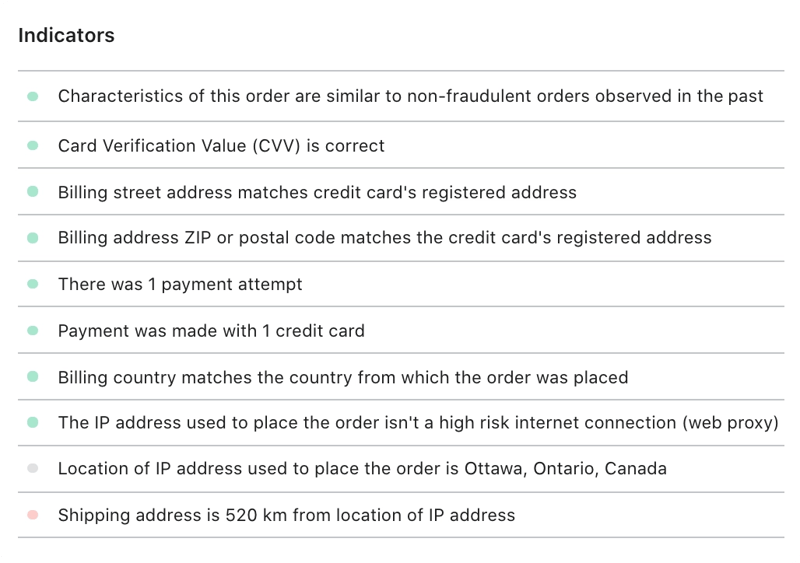

Businesses will want to investigate any order that they believe to be fraudulent or that Shopify has flagged with a warning symbol next to the order number. Look for the Fraud Analysis section on the order page to review the fraud indicators, which are marked in three colors:

- Green icons indicate the marked information appears legitimate.

- Grey icons flag data that can be used to evaluate the legitimacy of an order.

- Red icons mark order information that’s usually associated with fraudulent activity.

Source: Shopify

Businesses should remember that these indicators don’t calculate how likely it is that an order is fraudulent; instead, they simply list what legitimate or suspected fraudulent activity Shopify identified during its fraud analysis. If you want to know how likely an order is to be fraudulent, then you should look at the order's fraud recommendation.

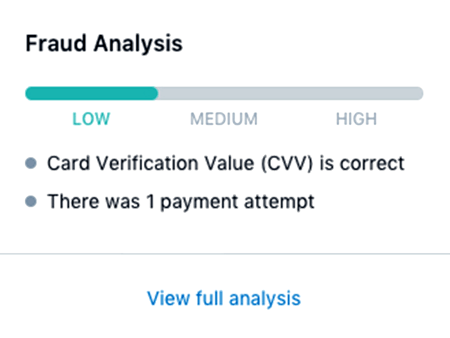

2. View the fraud recommendation

Businesses that are using Shopify Payments or are on the Shopify Plan or higher will see the fraud indicators plus a fraud recommendation for each of their orders.

Source: Shopify

This recommendation classifies an order’s chargeback risk as low, medium, or high and then flags medium- and high-risk orders on the Orders page. These rankings give businesses added insights that can help them make their transaction decisions.

To develop these recommendations, Shopify applies machine learning algorithms to its historical database of transactions across all Shopify stores and identifies fraud trends and patterns. To help protect businesses against emerging threats, Shopify continuously updates these algorithms based on new fraud information and reports from businesses.

3. Analyze third-party app recommendations

If a business is using a third-party fraud app, that app’s transaction indicators and recommendations display alongside Shopify's fraud analysis for each order.

What Are High-Risk Businesses?

How does a business earn the label as a “high-risk” merchant? There are a few ways.

You could be located in a high-risk region. Some parts of the world are more fraud-prone, due to lax regulations, high crime, or other factors. Nigeria, the Philippines and Russia are on the Top 10 list of internet scamming countries. That means where you do business can be a red flag for card issuers.

Or the industry you’re in and/or products you sell could be a constant target for fraudsters or the industry itself could be highly controversial. For example, fashion and luxury goods, gaming, or cannabis and CBD. There may also be an issue with regulatory requirements.

Ecommerce businesses that are considered high-risk can’t open traditional merchant accounts. Instead, they must secure high-risk merchant accounts, which are subject to additional fees and conditions.

Shopify and High-Risk Transactions

Shopify offers additional fraud detection and prevention tools through their own payment processing gateway, Shopify Payments. However, Shopify Payments is only available to stores that operate in certain countries and regions – notably excluding many countries that fall in the high-risk category.

Also, before signing up for Shopify Payments, you’ll need to confirm your business type and products aren't prohibited by the terms of service, another possible hurdle for a high-risk merchant.

Even with all the best protections Shopify or third-party apps have to offer, some high-risk orders can slip through the Shopify platform and be approved. And unfortunately, they may result in costly chargebacks.

Shopify and Chargebacks

Activating ShopPay, Shopify’s accelerated, one-tap checkout tool, gives shop owners access to Shopify Protect. This feature is available for free and helps protect eligible orders against fraudulent and unrecognized chargebacks.

Shopify Protect will mark an order as “protected” if it detects an at-risk transaction. And if a chargeback is then filed on that protected order, Shopify will reimburse the business for the chargeback and manage the entire chargeback dispute process.

If a fraudulent chargeback is made on an order that isn't “protected” (and there are a number of reasons why that can happen), the disputed amount and the chargeback fee aren't reimbursed to you unless the credit card company resolves the dispute in your favor.

Merchants may need extra help in preventing — or winning — chargeback disputes. That’s why Shopify has grouped the myriad chargeback reason codes among the card networks into these eight categories and has outlined the documentation needed to increase a merchant’s chances of winning chargeback disputes.

1. Fraud

Customers will file fraud chargebacks when their credit card has been lost or stolen and unauthorized purchases have been made.

To strengthen their representment case, businesses should submit proof of delivery, like a signature on a delivery form or the identification details of the individual who signed for the delivery. If businesses can demonstrate that the cardholder has or is using the merchandise in question, that evidence should also be submitted.

2. Unrecognized purchase

If the customer doesn’t recognize the business descriptor or the transaction on their billing statement, they might file a dispute.

Businesses can prevent these chargebacks from being successful by ensuring the company descriptor that displays on card statements is clear and recognizable to customers and by providing proof of the transaction, including order confirmations and email communications.

3. Duplicate purchases

When a customer is charged twice for the same transaction, they may opt to file a chargeback instead of calling customer service for a refund.

If businesses notice that a customer was double-billed for a purchase, they should immediately refund one of the transactions and notify the customer about the mistake.

4. Recurring subscriptions

Customers may forget they signed up for a recurring subscription and didn’t see the reminder notice (if the business sent one) — or they might think they cancelled their subscription before the next billing cycle.

In this scenario, avoid a chargeback completely by canceling the subscription immediately. But businesses who pursue representment should provide documentation of their subscription and cancellation policies and proof that the customer agreed to them both. Businesses might also submit proof that customers used or accessed a product after they claimed to have cancelled their subscription.

5. Product not received

After claiming they didn’t receive the goods or services they ordered and paid for, customers may file a chargeback on the transaction.

While packages are occasionally lost in transit, businesses can bolster their case by submitting tracking numbers, shipping addresses, proof of delivery (or, in the case of digital goods, proof they were downloaded or accessed). Businesses should provide customers with regular shipping updates, including estimated delivery dates.

6. Product is unacceptable

The customer claims the item arrived damaged or defective or the delivered product was not as described.

To win this type of chargeback dispute, businesses should demonstrate the pictures and descriptions online match the actual product, and they should ensure the product is packed to minimize the risk of shipping damage.

7. Credit not issued

The customer files a chargeback because they’ve returned the product or cancelled their order, but the business hasn’t issued a credit.

If the cancellation or return was outside a business’s return, refund or exchange policy, businesses should submit a clear copy of the policies in their representment documentation.

8. General

This is the catch-all category for chargebacks that don’t fit into any of the other categories.

To successfully defend themselves, businesses should research the specific chargeback reason code with the credit card issuer.

Clearly, preventing and disputing chargebacks is time-consuming, and it’s not an activity that contributes to an online business’s bottom line. Even with all the fraud tools Shopify provides, businesses may decide they want the additional protection that an experienced partner can provide.

So, what should you look for?

A Comprehensive Approach to Chargeback Prevention

Like Goldilocks, you want a chargeback prevention solution that is “just right.”

Most solutions combine fraud filters that either decline or flag potentially “bad” orders with an additional review of those flagged orders by a trained fraud analyst or whoever is available. These purely automatic solutions create a false sense of security because companies aren’t necessarily “seeing” the fraud. Then there is the impact on the customer.

If your fraud filters and automated rules are too strict, you’re undoubtedly declining orders from good customers. Declining good customers, especially new customers who’d you like to be returning customers, creates an even bigger problem for ecommerce businesses.

These types of solutions demand a balancing act on the part of the business, searching for a middle ground between expensive chargebacks and unhappy customers. That’s where the hard-won expertise of a chargeback prevention partner can be a relief.

Hybrid approach to fraud protection

At ClearSale, we use a hybrid approach, emphasizing the quick approval of nearly all legitimate transactions while rejecting transactions that are clearly fraudulent. Our AI-driven technology incorporates an auto-approval algorithm, effectively clearing 97% of orders. Approximately 3% are selected for a secondary review conducted by our skilled fraud analysts. This team gathers insights from these evaluations and integrates this knowledge back into our approval algorithm, continually refining its accuracy.

This enables us to provide instant decisions to our clients. Secondary reviews increase accuracy and speed up decision-making, enhancing the overall customer experience. The result: Our clients see lower chargebacks, lower false declines and higher approval rates.

By conducting secondary reviews, we ensure added protection for your customers, who depend on your platform for a safe and secure shopping experience. This approach makes secondary reviews frictionless, ultimately serving the interests of both your customers and your business.

ClearSale Chargeback Prevention and Management

Even with a highly effective fraud prevention solution, your business may experience some chargebacks. For those instances, you should consider a comprehensive chargeback protection and management solution.

At ClearSale, we offer clients three options.

ClearSale Total Protection

For large businesses whose fraud teams have a good understanding of risk profiles and goals, our Total Protection approach allows you to recoup a portion of any losses due to fraudulent transactions.

We’ll establish a Service Level Agreement (SLA) that specifies KPI thresholds related to fraud and chargebacks. And we’ll reconcile to those KPIs every quarter. If they aren’t met, you’ll receive a discounted invoice.

Companies that choose this approach aren’t directly reimbursed for chargebacks that may occur; however, they do benefit from our hybrid fraud prevention model that combines AI-enabled automatic approvals and secondary review by the world’s biggest and most experienced team of fraud experts.

ClearSale Total Guaranteed Protection

High-risk ecommerce businesses may choose our 100% guaranteed coverage approach to handling fraud-related chargebacks. This “chargeback insurance” guarantees that any approved transaction that turns out to be fraudulent and results in a chargeback will be reimbursed to you.

End-to-End Chargeback Management

Regardless of size, your ecommerce business may benefit most from comprehensive chargeback management that includes a chargeback reversal approach designed to recover financial losses.

With our acquisition of chargeback management provider ChargebackOps, we can offer companies chargeback mitigation and resolution services including:

- Training fraud analyst teams

- Conducting data audits and gathering compelling evidence

- Drafting timely responses to banks and card issuers

Where it makes sense, this approach also offers companies operational insights that can help improve internal processes that may be contributing to fraud risk and subsequent chargebacks.

From High-Risk to High Confidence

Choosing a customized chargeback management approach lets ecommerce businesses breathe a little easier. On a high-profile platform like Shopify that attracts the attention of fraudsters, owners want to be protected against the increase in fraud attempts and poised for long-term financial success.

The right partner can help businesses protect revenue against costly chargebacks while preventing costly false declines — and without a moment to lose. Thankfully, ClearSale’s solutions integrate quickly and easily with Shopify. And we have the proven experience to let you confidently accept more transactions without the risk of business-damaging chargebacks. Contact us today to learn how easy it is to get started.